Reaffirms Project’s Excellent Leverage To Rising Gold Prices

Increased 13.6 Million Ounce Resource Solidifies Standing As LargestIndependent Gold-Only Resource in North America

Annual Average Production of 306,200 Ounces per Year Over 21 Year Mine Life

Significantly De-Risks Project and Forms Solid Foundation To Advance Project Forward

Vancouver, British Columbia, November 4, 2021 – International Tower Hill Mines Ltd. (“ITH” or the “Company”) (TSX: ITH; NYSE-MKT: THM) today announced the results of the Pre-Feasibility Study (the “PFS”) for its Livengood Gold Project (the “Project”) located near Fairbanks, Alaska. The PFS details a project that would process 65,000 tons per day and produce 6.4 million ounces of gold over 21 years from a gold resource estimated at 13.6 million ounces at 0.60 g/tonne. The PFS utilized a third-party review by Whittle Consulting and BBA Inc. to integrate new interpretations based on an expanded geological database, improved geological modelling, new resource estimation methodology, an optimized mine plan and production schedule, additional detailed metallurgical work at various gold grades and grind sizes, changes in the target grind for the mill, new engineering estimates, and updated cost inputs, all of which significantly de-risk the Project. The PFS has estimated the capital costs of the Project (“CAPEX”) at US$1.93 billion, the total cost per ton milled (“OPEX”) at US$13.12, the all-in sustaining costs (“AISC”) at US$1,171 per ounce, and an after-tax NPV(5%) of US$400 million at $1,800/oz, US$975 million at US$2,000/oz, and US$2.3 billion at $US2,500/oz.

“This PFS confirms that the Livengood Gold Project is the one of the largest, highly leveraged gold projects in North America. This study is the culmination of years of work and greatly enhances our understanding of the deposit. We have now thoroughly evaluated, optimized, and de-risked all major elements of the Project and have an excellent foundation on which to build shareholder value. International Tower Hill’s estimated 13.6 million ounces, together with our favorable jurisdiction and proximity to infrastructure, offers our investors great leverage to the gold price.” said Karl Hanneman, CEO.

The Company invites you to attend a conference call and webcast hosted by CEO Karl Hanneman to discuss the Company and this news release.

Conference Call & Webcast Details:

Pre-Feasibility Study Overview

The Project configuration evaluated in the PFS is a conventional, owner-operated surface mine that will utilize large-scale mining equipment in a blast/load/haul operation. Mill feed would be processed in a 65,000 tons per day comminution circuit consisting of primary and secondary crushing, wet grinding in a single semi-autogenous (SAG) mill and single ball mill followed by a gravity gold circuit and a conventional carbon in leach (CIL) circuit.

Whittle Enterprise Optimization

Prior to beginning the PFS, the Company retained Whittle Engineering and BBA Engineering to collaborate on an enterprise optimization study (the “Whittle and BBA Study”) to review various technologies and project configurations and to recommend the optimum configuration for the PFS. The Whittle and BBA Study reviewed secondary crushing with SAG and ball mill, tertiary crushing with ball mill, gravity/CIL at P80 of 90 micron to 250 micron, stand-alone and auxiliary heap leach configurations, gravity only gold recovery, gravity/flotation with pressure oxidation and CIL of flotation concentrate. These configurations were evaluated at various combinations of project ramp up strategy, annual throughput, primary, secondary, and tertiary grind size, as well as mining fleet size and stockpile management strategies. Tailings technologies reviewed included conventional tailings and pressure filtered tailings.

The Whittle and BBA Study determined that the gravity/CIL plant at P80 250 micron with conventional tailings provided the highest NPV, which is the configuration detailed in the PFS.

Pre-Feasibility Study Summary

The PFS was prepared by independent third-party consultants and provides information on the optimized Project with higher throughput, an updated resource estimate, and capital and operating cost estimates as compared to the project evaluated in the National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) April 2017 Technical Report (the “2017 Report”). The final version of the NI 43-101 technical report containing the PFS will be filed on SEDAR within 45 days. As a result of the changes to the Project as evaluated in the PFS, including differences in the mineral resource estimation methodology and changes to the economic parameters applied to the geologic block model (gold price, recovery, CAPEX, and OPEX), all of which resulted in a change in the mineral resources, the Project as evaluated in the 2017 Report is no longer considered current and the 2017 Report should therefore not be relied upon by investors.

The Company cautions that the PFS is preliminary in nature, and is based on technical and economic assumptions which would be further refined and evaluated in a full feasibility study. The PFS is based on an updated Project mineral resource estimate effective as of August 20, 2021 using a different mineral resource model than what was used in the 2017 Report.

The following is a summary of the material aspects and assumptions of the PFS. Investors are urged to review the complete NI 43-101 report following its filing on SEDAR for complete details of the PFS.

The engineering design to estimate capital costs used in the PFS are within a -20%/+25% accuracy.

Project Location

The Project is connected by an existing paved highway to the city of Fairbanks, 70 miles to the southwest in central Alaska. The Project is located in an active mining district that has been mined for gold since 1914. The State of Alaska land use plan designates mining as the primary surface land use for the area in which the Project is located. Employees would be bussed daily to the site from Fairbanks.

Infrastructure

The Project would include a lined tailings management facility, an administration office/shop/warehouse complex, and would also include construction of a 50-mile 230kV electrical transmission line to the mine site from the existing grid power near Fairbanks, Alaska.

Environmental and Community Relations

Twelve continuous years of baseline environmental work continues to indicate that all aspects of the Project can be successfully and safely managed. The design of the tailings facility incorporates best practices including a lined rock fill structure with a lined tailings basin. The Project development team has considerable experience working with Alaska’s large mine permitting process and has a proven and respected track record of developing mining projects safely and in an environmentally sound manner. The Project has already and will continue to provide local economic opportunities with local access to a highly skilled and available work force. The Company is also working to seek early input on the Project and to explore ways to maximize economic benefits to the local communities.

Summary of Results of the 65,000 Tons Per Day PFS

| OPERATING METRICS |

2021 PFS |

|

| Mill Throughput |

65,000 |

tons/day |

| Head Grade – Year 1-5(1) |

0.79 |

g/tonne |

| Head Grade – LOM(1) |

0.65 |

g/tonne |

| Gold Recovery – LOM |

71.4 |

% |

| Mine Life |

21 |

years |

| Total Ounces Produced |

6,430,178 |

Troy ounces |

| Average Annual Production – Year 1-5 |

388,600 |

Troy ounces |

| Average Annual Production – LOM |

306,200 |

Troy ounces |

| Total Ore Processed |

474 |

Million tons |

| Total Waste(2) |

547 |

Million tons |

| Annual Mining Rate |

52 |

Million tons |

| Waste Rock to Mill Ore (ton) Ratio – LOM during production |

0.98:1 |

Waste to Ore |

| Waste Rock to Mill Ore (ton) Ratio – LOM |

1.15:1 |

Waste to Ore |

| Low Grade Stockpile – Total Placed/Maximum Size |

105/88 |

Million tons |

(1) Diluted grade

(2) Includes 84 million tons pre-production

| FINANCIAL METRICS |

2021 PFS |

US$ |

| CAPEX – Initial |

1.93 |

$Billion |

| CAPEX – Sustaining |

658 |

$Million |

| Reclamation & Closure |

322 |

$Million |

| OPEX – Mining |

2.05 |

$/ton mined |

| OPEX – Processing |

7.72 |

$/ton ore |

| OPEX – General &Administrative (G&A) |

1.35 |

$/ton ore |

| OPEX - Operating Cost – Year 1-5 |

887 |

$/Ounce |

| OPEX - Operating Cost – LOM |

1,068 |

$/Ounce |

| All-In Sustaining Cost of Production – Year 1-5 |

1,038 |

$/Ounce |

| All-In Sustaining Cost of Production – LOM |

1,171 |

$/Ounce |

Gold Price Sensitivity Analysis

The following table shows the average annual free cash flow and EBIDTA generated by the Project at various gold prices.

| (US$M) |

FREE CASH FLOW |

EBIDTA |

| Gold Price ($/Oz) |

Average Annual (Year 1-5) |

Average Annual (LOM) |

Average Annual (Year 1-5) |

Average Annual (LOM) |

| $1,500 |

$159 |

$108 |

$229 |

$142 |

| $1,680 (PFS Base Case |

$225 |

$154 |

$296 |

$197 |

| $1,800 |

$269 |

$184 |

$342 |

$234 |

| $2,000 |

$332 |

$232 |

$417 |

$295 |

| $2,500 |

$482 |

$349 |

$605 |

$449 |

The following table shows the after-tax economics at various gold prices.

| Gold Price ($/Oz) |

AFTER TAX NPV 0% ($M) |

AFTER TAX NPV 5% ($M) |

IRR (%) |

Payback (Years) |

| $1,500 |

$202 |

($512) |

1.00% |

16.2 |

| $1,680 (PFS Base Case) |

$1,137 |

$45 |

5.30% |

10.4 |

| $1,800 |

$1,741 |

$400 |

7.70% |

8.2 |

| $2,000 |

$2,729 |

$975 |

11.20% |

6.3 |

| $2,500 |

$5,102 |

$2,351 |

18.50% |

3.9 |

Capital Costs

Key capital expenditures for initial and sustaining capital requirements are identified in the following table.

| |

US$ Million |

| Description |

Initial |

Sustaining |

| Process Facilities |

$433 |

|

| Infrastructure Facilities |

459 |

$514 |

| Power Supply |

87 |

|

| Mine Equipment |

200 |

139 |

| Mine Development |

230 |

|

| Owners Costs |

296 |

5 |

| Contingency |

220 |

|

| Total |

$1,925 |

$658 |

Rounding of some figures may lead to minor discrepancies in totals.

All-in Sustaining Costs

The table below highlights the all-in sustaining costs and the all-in cost over the life of the Project:

| |

Year 1-5 |

LOM |

| |

US$/Ounce |

US$ Million |

US$/Ounce |

US$ Million |

| Operating Costs |

$887 |

$1,724 |

$1,068 |

$6,870 |

| Sustaining Capital Expenditures |

151 |

292 |

102 |

658 |

| All-In Sustaining Costs(1) |

$1,038 |

$2,016 |

$1,171 |

$7,529 |

| Capital Expenditures (2) (3) |

0 |

0 |

299 |

1,925 |

| Funding of Reclamation Trust Fund (4) |

30 |

58 |

42 |

268 |

| All-In Costs(1) |

$1,068 |

$2,075 |

$1,512 |

$9,722 |

Rounding of some figures may lead to minor discrepancies in totals.

- All-In Sustaining Costs and All-In-Costs are non-IFRS measures. See reference to “Non-IFRS Measures” below.

- Includes initial capital expenditures only.

- Excludes US$40 million of recoverable initial stores inventory.

- Total US$322 million estimated costs.

Annual Gold Production

The chart below highlights the anticipated production schedule. Total life-of-mine production is anticipated to be 6,430,178 ounces. Mill feed will consist of reclaimed ore from the low-grade stockpile during Years 18 through 21.

| Year |

Mill Feed Grade (g/tonne) |

Ounces Produced (000) |

| 1 |

0.76 |

321 |

| 2 |

0.69 |

388 |

| 3 |

0.93 |

482 |

| 4 |

0.93 |

437 |

| 5 |

0.61 |

314 |

| 6 |

0.61 |

328 |

| 7 |

0.64 |

340 |

| 8 |

0.64 |

329 |

| 9 |

0.69 |

357 |

| 10 |

0.58 |

306 |

| 11 |

0.61 |

296 |

| 12 |

0.72 |

336 |

| 13 |

0.77 |

339 |

| 14 |

0.77 |

322 |

| 15 |

0.71 |

308 |

| 16 |

0.73 |

316 |

| 17 |

0.65 |

293 |

| 18 |

0.36 |

188 |

| 19 |

0.36 |

188 |

| 20 |

0.36 |

188 |

| 21 |

0.37 |

54 |

| LOM |

0.65 |

6,430 |

Rounding of some figures may lead to minor discrepancies in totals.

Project Mineral Reserves

The table below presents the Mineral Reserve estimate for the Project (effective as of October 22, 2021). These Proven and Probable Mineral Reserves formed the basis of the economic evaluation of the Project and are based on a gold price of US$1,680 per ounce. The economic assumptions and parameters used for the calculation of reserves are the same as those used for the PFS financial model. Note that tonnages presented are in the metric system.

Livengood Gold Project Mineral Reserve Estimate

| Classification |

Tonnes (Mt) |

Au (g/tonne) |

Contained Au (000’s) |

| Proven |

411.5 |

0.64 |

8,492 |

| Probable |

18.5 |

0.86 |

512 |

| Total P & P |

430.1 |

0.65 |

9,004 |

- Mineral Reserves are reported using the 2014 CIM Definition Standards and are estimated in accordance with 2019 CIM Best Practices Guidelines.

- Mineral Reserves are estimated using a gold price of US$1,680 per ounce, and consider a 3% royalty, 1.80/oz for smelting, refining, and transportation costs, and a gold payable of 99.9%

- Metallurgical recovery curves were developed for each rock type, with the Mineral Reserves having the following tonnage weighted averages; 83.3%, for Rocktype 4, 79.8% for Rocktype 5, 73.5% for Rocktype 6, 66.4% for Rocktype 7, 58.7% for Rocktype 8 and 57.1% for Rocktype 9, including 22% for massive stibnite mineralization.

- As a result of the complex metallurgical recovery equations, it is difficult to determine specific cut-off grades. The following presents the lowest gold grades for each rocktype that are processed in the life of mine plan; 0.26 g/t for Rocktype 4, 0.28 g/t for Rocktype 5, 0.31 g/t for Rocktype 6, 0.31 g/t for Rocktype 7 and 0.42 g/t for Rocktype 8 and 0.42 g/t for Rocktype 9.

- The strip ratio for the open pit is 1.2 to 1.

- The Mineral Reserves are inclusive of mining dilution and ore loss.

- The reference point for the Mineral Reserves is the primary crusher.

- Totals may not add due to rounding.

- The foregoing mineral reserves are based upon and are included within the current mineral resource estimate for the Project.

Project Mineral Resources

The mineral resource estimates set forth in the PFS (“2021 MRE”) have been prepared by Resource Development Associates Inc. (“RDA”). Compared to the mineral resource estimates in the 2017 Report, the 2021 MRE included spatial modelling of the occurrence of antimony throughout the deposit as well as modelling of the locations of massive stibnite veins within the deposit. These details add valuable contributions to the reasonable prospects of eventual economic extraction of gold for the Project. Gold mineralization has been interpolated into 10 x 10 x 10-meter blocks using inverse distance cubed (ID3) estimation techniques, believed to more conservatively support future production schedules as compared to the 2017 Report, which was based on Multiple Indicator Kriging of 15 x 15 x 10-meter blocks parceled into 7.5 x 7.5 x 10-meter selective mining units.

Table 1 Mineral Resource Estimate – Open Pit Constrained – Economic Parameters at Gold Selling Price of US$1,650 per Troy Ounce. Resources Estimated at Variable Au Cutoff Grades – as described in Table 2

(Qualified Person: Scott Wilson CPG; Effective August 20, 2021)

| Classification |

Tonnes (Mt) |

Au (g/t) |

Contained Au (000’s) |

| Measured |

646.0 |

0.60 |

12,482 |

| Indicated |

58.5 |

0.61 |

1,142 |

| Total M & I |

704.5 |

0.60 |

13,624 |

| Inferred |

16.0 |

0.40 |

207 |

Mineral resources for the Project were determined based upon a combination of 776 reverse circulation and diamond drillholes comprising 147,658 assays of which 125,450 assays measured detectable Au mineralization. High grade Au outliers were capped prior to compositing. Assays were composited to nominal ten-meter lengths, yielding 20,806 individual samples which were used for the estimation of mineralization. Mineralization was determined using inverse distance cubed estimation techniques, adhering to geological constraints throughout the mineral deposit.

In order to define the quantities of Au with “reasonable prospects for economic extraction” by open pit methods, RDA determined pit constraining limits using the Lerchs-Grossman© economic algorithm which constructs lists of related blocks that should or should not be mined. The final list defines a surface pit shell that has the highest possible total value, while honoring the required surface mine slope and economic parameters. Mineral resources were determined at a gold selling price of US$1,650.

The parameters listed in Table 2 define a realistic basis to estimate the mineral resources for the Project and are based on the extensive scientific, metallurgical and engineering based analyses that have been completed by Tower Hill Mines since 2006. Mineral resources for the Project have been limited to mineralized material that occurs within the pit shells and which could be scheduled to be processed based on the defined cut-off grades. All other material within the constraining pit, which was not classified according to CIM Definition Standards, was characterized as non-mineralized material.

Table 2 Pit Constraining Parameters

| Parameter |

Unit |

Rock

Type 4 |

Rock

Type

5 |

Rock

Type

6 |

Rock

Type

7 |

Rock

Type

8 |

Rock

Type

9 |

| Mining Cost Unprocessed Rock |

US$/tonne |

1.76 |

1.74 |

1.74 |

1.68 |

1.76 |

1.76 |

| Processing Cost |

US$/ process tonne |

9.27 |

9.15 |

9.17 |

9.50 |

9.71 |

9.71 |

| G & A |

US$/process tonne |

1.55 |

1.55 |

1.55 |

1.55 |

1.55 |

1.55 |

| Au Recovery |

Avg %1 |

84 |

80 |

71 |

67 |

55 |

56 |

| Royalty |

% |

3 |

3 |

3 |

3 |

3 |

3 |

| Au Selling Price |

US$/oz |

1,650 |

1,650 |

1,650 |

1,650 |

1,650 |

1,650 |

| Au Cut-Off |

g/tonne |

0.21 |

0.20 |

0.25 |

0.25 |

0.33 |

0.33 |

| Overall Slope Angle |

Degrees |

45 |

45 |

45 |

45 |

45 |

45 |

1 Average % Au Recovery includes massive stibnite at 22% recovery

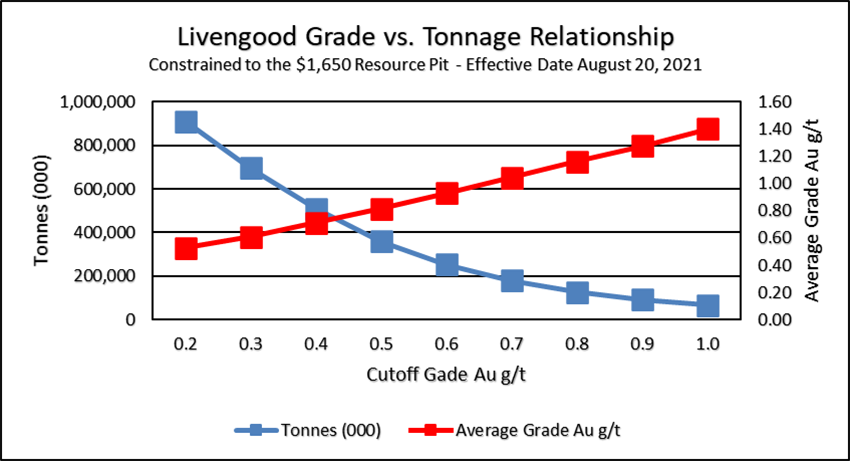

Grade and Tonnage Sensitivity to Cutoff Grade

Mineral resources at Livengood are sensitive to the selection of the reporting cutoff grade. To illustrate this sensitivity, the block model quantities and grade estimates within the constraining pit are presented in Table 3 at linear increases in the cutoff grades for measured, indicated and inferred mineral resources at Livengood. The same results are presented graphically in Figure 1. Mineralization is constrained to the pit using the parameters in Table 2. The numbers presented in Table 3 should not be misconstrued with a mineral resource statement. The figures are only presented to show the sensitivity of block model estimates to the selection of a cutoff grade. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

Table 3 Sensitivity of Mineral Resources to cutoff used. Effective Date: August 20, 2021.

QP Scott Wilson CPG

| |

Measured |

Indicated |

Measured & Indicated |

Inferred |

| Cutoff Au g/t |

Tonnes (000) |

Grade Au g/t |

Au Oz. (000) |

Tonnes (000) |

Grade Au g/t |

Au Oz. (000) |

Tonnes (000) |

Grade Au g/t |

Au Oz. (000) |

Tonnes (000) |

Grade Au g/t |

Au Oz. (000) |

| 0.2 |

816,569 |

0.53 |

13,914 |

73,263 |

0.53 |

1,248 |

889,832 |

0.53 |

15,162 |

20,423 |

0.37 |

243 |

| 0.3 |

626,843 |

0.61 |

12,293 |

55,069 |

0.63 |

1,115 |

681,912 |

0.61 |

13,409 |

13,359 |

0.43 |

185 |

| 0.4 |

464,710 |

0.71 |

10,608 |

37,347 |

0.76 |

913 |

502,057 |

0.71 |

11,520 |

6,017 |

0.52 |

101 |

| 0.5 |

332,891 |

0.81 |

8,669 |

25,437 |

0.91 |

744 |

358,328 |

0.82 |

9,413 |

2,142 |

0.65 |

45 |

| 0.6 |

234,524 |

0.92 |

6,937 |

17,976 |

1.06 |

613 |

252,500 |

0.93 |

7,549 |

1,079 |

0.75 |

26 |

| 0.7 |

164,938 |

1.03 |

5,462 |

13,645 |

1.19 |

522 |

178,583 |

1.04 |

5,984 |

614 |

0.84 |

17 |

| 0.8 |

117,098 |

1.15 |

4,329 |

10,648 |

1.31 |

448 |

127,746 |

1.16 |

4,778 |

335 |

0.92 |

10 |

| 0.9 |

83,825 |

1.26 |

3,396 |

8,372 |

1.44 |

388 |

92,197 |

1.28 |

3,783 |

180 |

0.98 |

6 |

| 1.0 |

61,474 |

1.38 |

2,727 |

6,479 |

1.58 |

329 |

67,953 |

1.40 |

3,057 |

59 |

1.04 |

2 |

Figure 1 Sensitivity of Mineral Resources to cutoff used. Effective Date: August 20, 2021. QP Scott Wilson CPG

Sensitivity of Mineralization to Gold Price

The sensitivity of the Livengood Project mineralization to the gold price was performed at selling prices of US$1,320/oz (- 20%),US $1,650/oz (the 2021 MRE selling price) and US$1,980/oz (+ 20%). The input technical parameters, defined in Table 2, were used in the analysis.

Table 4 Sensitivity of Pit-Constrained Mineralization Inventory at Gold Prices +/- 20% of US$1,650

| WhittleTM Pit Gold Price |

Classification |

Tonnes (Mt) |

Au (g/t) |

Contained Au (000’s) |

| US$1,320 |

Measured |

423.84 |

0.70 |

9,496.30 |

| Indicated |

24.35 |

0.85 |

666.13 |

| Total M & I |

448.19 |

0.71 |

10,162.43 |

| Inferred |

2.02 |

0.11 |

7.15 |

| US$1,650 |

Measured |

646.00 |

0.60 |

12,482.49 |

| Indicated |

58.51 |

0.61 |

1,141.61 |

| Total M & I |

704.51 |

0.60 |

13,624.10 |

| Inferred |

15.98 |

0.40 |

206.98 |

| US$1,980 |

Measured |

845.60 |

0.54 |

14,668.81 |

| Indicated |

108.98 |

0.49 |

1,717.27 |

| Total M & I |

954.58 |

0.53 |

16,386.08 |

| Inferred |

31.97 |

0.37 |

377.99 |

The mineral resource estimate for the Project is inclusive of the mineral reserves for the Project. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral resource estimates do not account for mineability, selectivity, mining loss and dilution. These mineral resource estimates include inferred mineral resources that are normally considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. There is also no certainty that these inferred mineral resources will be converted to measured and indicated categories through further drilling, or into mineral reserves, once economic considerations are applied.

Metallurgy Recovery by Rock Type

The Company has completed extensive metallurgical test work on the rock types that comprise the current estimated mineral resource. Recovery rates by rock type using gravity and carbon-in-leach recovery of gravity tail are shown in the table below:

| Rock Type |

Gold Recovery %1 |

| RT4 Cambrian |

83.3 |

| RT5 Sunshine Upper Sediments |

79.8 |

| RT6 Upper Sediments |

73.5 |

| RT7 Lower Sediments |

66.4 |

| RT8 Volcanics-Sunshine Zone |

58.7 |

| RT9 Volcanics-Core Zone |

57.1 |

- Weighted average recovery within reserve pit at p80 250 micron based on Au grade/geologic domain/Sb concentration/massive stibnite occurrence.

Detailed Report

A NI 43-101 compliant technical report that summarizes the results of the PFS will be filed on SEDAR at www.sedar.com within 45 days of this news release and will be available on the Company’s website www.ithmines.com at that time.

Qualified Persons

The PFS was prepared by the following Qualified Persons (as defined under NI 43-101), each of whom is independent of the Company under NI 43-101, and each of whom has reviewed, verified, and approved the scientific and technical data for which they have responsibility contained in this news release pertaining to the PFS. No limitations were imposed on the verification process.

| Qualified Person |

Company |

Scope of Responsibility |

| Colin Hardie, P. Eng (Ontario APEO No. 90512500) |

BBA Inc. |

Financial model, Process Plant and Infrastructure CAPEX, G&A OPEX, Environmental Studies and Permitting, Overall NI 43-101 Integration |

| Jeffrey Cassoff, P. Eng. (Quebec OIQ No. 5002252) |

BBA Inc. |

Mineral Reserves |

| Mélanie Turgeon, Eng. (Quebec OIQ No. 5028478) |

BBA Inc. |

Process Engineering and Process Plant OPEX, Mineral Processing and Metallurgical Testing |

| Ryan T. Baker. (Nevada No. 11172) |

NewFields Companies, LLC |

Geotechnical Engineering, Waste Rock and Water Management, TMF CAPEX |

| Mike Levy, P.E. (Colorado No. 40268) |

JDS Energy and Mining Inc. |

Mine Slope Stability |

| Scott Wilson, CPG #10965 |

Resource Development Associates Inc. |

Geology, Drilling, Resource Estimation |

Mr. Colin Hardie is a Senior Process Engineer and the Director of Non-Ferrous Metal Markets at BBA. He joined the BBA team in 2008 and has over 20 years of experience as an operations metallurgist, engineering consultant and in process research and development. He is a graduate of the University of Toronto with a Bachelor of Applied Science degree in Geological and Mineral Engineering (1996). Mr. Hardie also has a Master of Engineering degree in Metallurgy from McGill University (1999) as well as a Master Degree in Business Administration from HEC Montreal (2008). He is a registered Professional Engineer in the Province of Ontario, Canada. He has acted as a Qualified Person and lead study integrator for numerous North American gold, base metal and industrial mineral projects.

Mr. Jeffrey Cassoff is a Senior Mining Engineer and the Team Leader for Mining Engineering at BBA. Mr. Cassoff has over 20 years of experience in the mining industry working for both mining operations and as a consultant. Mr. Cassoff is a graduate of McGill University with a Bachelor of Mining Engineering (1999). Mr. Cassoff is a registered Professional Engineer in the province of Quebec, Canada. He has acted as a Qualified Person for numerous gold projects.

Mrs. Mélanie Turgeon is a Process Engineer at BBA and has worked in consulting engineering since 2013. She is a graduate of the Université de Sherbrooke with a Bachelor of Chemical Engineering (2011) and a registered Engineer in the province of Quebec, Canada. She has been involved in the development of metallurgical testwork campaigns and in the writing of technical reports in accordance with standards governing NI 43-101.

Mr. Ryan T. Baker is a Principal Engineer with NewFields Mining Design & Technical Services, LLC, located in Lone Tree, CO. He is a graduate of Colorado State University with a Bachelor of Science degree in Civil Engineering (1993) and a registered Professional Engineer in Nevada (#13947), Alaska (#11172), Idaho (#10226), Colorado (#36988), Missouri (PE2008000049), and New Mexico (#22110). He is also a Registered Member of the Society for Mining, Metallurgy, and Exploration (SME, #4204584) and the American Society of Civil Engineers (ASCE, #307827) with relevant experience pertaining to heap leach, tailings and mine overburden storage facilities, and mine surface infrastructure design and inspection since 1994.

Mr. Michael Levy is Geotechnical Manager with JDS Energy & Mining Inc. in Denver, CO. He is a graduate of the University of Iowa with a Bachelor of Science degree in Geology and a Master of Science degree in Civil-Geotechnical Engineering. He is a registered Professional Engineer with the states of Colorado (#40268) and a current member of the International Society for Rock Mechanics (ISRM) and the American Society of Civil Engineers (ASCE). Mike has practiced for 22 years and has undertaken numerous mining and civil geotechnical projects ranging from conceptual through feasibility design levels, mine construction and operations support. He is skilled in both soil and rock mechanics engineering and specializes in the design and management of underground and open pit mine excavations.

Mr. Scott E. Wilson, CPG (10965), Registered Member of SME (4025107) and President of Resource Development Associates Inc., is an independent consulting geologist specializing in mineral reserve and resource calculation reporting, mining project analysis and due diligence evaluations. He is acting as the Qualified Person, as defined in NI 43-101, and is an author of the technical report which will be filed by the Company for the mineral resource estimate and has reviewed and approved the mineral resource estimate and the PFS summarized in this news release. Mr. Wilson has over 32 years of experience in surface mining, resource estimation and strategic mine planning. Mr. Wilson is independent of the Company under NI 43-101.

On behalf of

International Tower Hill Mines Ltd.

(signed) Karl Hanneman

Chief Executive Officer

Contact Information: Richard J. Solie, Manager - Investor Relations

E-mail: [email protected]

Direct line: 907-328-2825

Toll-Free: 855-428-2825

Cautionary Note Regarding Forward-Looking Statements

This press release contains forward-looking statements and forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable Canadian and US securities legislation. All statements, other than statements of historical fact, included herein, including statements with respect to the mine plan, economic analysis (including capital expenditures, operating expenditures, all-in-sustaining costs and all-in costs) and production and design details described in the PFS; the potential to convert mineral resources to mineral reserves; additional optimization and exploration efforts and the results thereof; the ability of the Company to satisfy the derivative liability and the consequences of any failure to do so; the ability of the Company to potentially include refined and updated results in a subsequent full feasibility study; the ability of the Company to advance environmental baseline work in support of future permitting; the ability of the Company to advance the Livengood Project either as projected or at all; the potential for the Company to make a construction decision, whether when warranted by market conditions or at all; the potential for market conditions to be such that they warrant the making of a production decision; the potential development of any mine at the Livengood Project; business and financing plans and business trends are forward-looking statements. Information concerning mineral reserve/resource estimates and the economic analysis thereof contained in the PFS also may be deemed to be forward-looking statements in that it reflects a prediction of the mineralization that would be encountered, and the results of mining it, if a mineral deposit were developed and mined. Although the Company believes that such statements are reasonable, it can give no assurance that such expectations will prove to be correct. Forward-looking statements are typically identified by words such as: believe, expect, anticipate, intend, estimate, postulate, proposed, planned, potential and similar expressions, or are those, which, by their nature, refer to future events. The Company cautions investors that any forward-looking statements by the Company are not guarantees of future results or performance, and that actual results may differ materially from those in forward looking statements as a result of various factors, including, but not limited to, variations in the nature, quality and quantity of any mineral deposits that may be located, variations in the market price of any mineral products the Company may produce or plan to produce, the inability of the Company to obtain any necessary permits, consents or authorizations required for its activities, the inability of the Company to produce minerals from its properties successfully or profitably, to continue its projected growth, to raise the necessary capital (including, as required, to satisfy the derivative liability) or to be fully able to implement its business strategies, and other risks and uncertainties disclosed in the Company’s Annual Information Form filed with certain securities commissions in Canada and the Company’s annual report on Form 10-K filed with the United States Securities and Exchange Commission (the “SEC”), and other information released by the Company and filed with the appropriate regulatory agencies. All of the Company’s Canadian public disclosure filings may be accessed via www.sedar.com and its United States public disclosure filings may be accessed via www.sec.gov, and readers are urged to review these materials, including the 2017 Report and the technical report to be filed with respect to the Company’s Livengood property within 45 days hereof.

Non-IFRS Measures

The Company has included certain non-IFRS measures in this news release, as discussed below. The Company believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provides investors with an improved ability to evaluate the underlying performance of the Company. These non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures do not have any standardized meaning prescribed under IFRS, and therefore may not be comparable to other issuers.

All-In Sustaining Costs (“AISC”) and AISC/oz

AISC is a performance measure that reflects the expenditures that are required to produce an ounce of gold from current operations. While there is no standardized meaning of the measure across the industry, the Company’s definition is derived from the definition, as set out by the World Gold Council in its guidance dated June 27, 2013 and November 16, 2018, respectively. The World Gold Council is a non-regulatory, non-profit organization established in 1987 whose members include global senior mining companies. The Company believes that this measure is useful to external users in assessing operating performance and the ability to generate free cash flow from operations. The Company defines AISC as the sum of total cash costs, sustaining capital (capital required to maintain current operations at existing production levels), capital lease repayments, exploration expenditures designed to increase resource confidence at producing mines, amortization of asset retirement costs and rehabilitation accretion related to current operations. AISC excludes general corporate and administrative costs incurred at the non-project level, capital expenditures for significant improvements at existing operations deemed to be expansionary in nature, exploration and evaluation related to resource growth, rehabilitation accretion not related to current operations, financing costs, debt repayments, and taxes. Total AISC is divided by gold ounces sold to arrive at a per ounce figure.

All-In Costs (“AIC”) and All-In-Costs/oz

The Company defines AIC as the sum of AISC costs plus initial capital expenditures. Total AIC is divided by gold ounces sold to arrive at a per ounce figure.

Cautionary Note Regarding References to Resources and Reserves

National Instrument 43101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all resource and reserve estimates contained in or incorporated by reference in this news release have been prepared in accordance with NI 43-101 and the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resource and Mineral Reserves, adopted by the CIM Council on May 10, 2014 (the “CIM Standards”) as they may be amended from time to time by the CIM.

Accordingly, information in this press release providing descriptions of the Company’s mineral deposits in accordance with NI 43-101 may not be comparable to similar information made public by other U.S. companies subject to the United States federal securities laws and the rules and regulations thereunder.

Pursuant to CIM Definition Standards, "Inferred mineral resources" are that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Such geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resource and must not be converted to a mineral reserve. However, it is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource is economically or legally mineable. Disclosure of "contained ounces" in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute "reserves" by SEC standards as in place tonnage and grade without reference to unit measures.

Effective February 25, 2019, the SEC adopted new mining disclosure rules under subpart 1300 of Regulation S-K of the United States Securities Act of 1933, as amended (the "SEC Modernization Rules"), with compliance required for the first fiscal year beginning on or after January 1, 2021. The SEC Modernization Rules replace the historical property disclosure requirements included in SEC Industry Guide 7. As a result of the adoption of the SEC Modernization Rules, the SEC now recognizes estimates of "Measured Mineral Resources", "Indicated Mineral Resources" and "Inferred Mineral Resources". In addition, the SEC has amended its definitions of "Proven Mineral Reserves" and "Probable Mineral Reserves" to be substantially similar to corresponding definitions under the CIM Definition Standards. While the SEC Modernization Rules are purported to be "substantially similar" to the CIM Definition Standards, readers are cautioned that there are differences between the SEC Modernization Rules and the CIM Definitions Standards. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as "proven mineral reserves", "probable mineral reserves", "measured mineral resources", "indicated mineral resources" and "inferred mineral resources" under NI 43-101 would be the same had the Company prepared the reserve or resource estimates under the standards adopted under the SEC Modernization Rules.

This news release is not, and is not to be construed in any way as, an offer to buy or sell securities in the United States.