| |

Low Capex Accelerated Heap Option: NPV(5%) $579M, IRR 26.9%,

Producing 513,000 ounces of gold/year

Upscale Milling-Heap Option: NPV(5%) $1.11B, IRR 18.5%,

Producing 833,000 ounces of gold/year

Vancouver, B.C.......International Tower Hill Mines Ltd. ("ITH" or the "Company") - (TSX: ITH, NYSE-A: THM, Frankfurt: IW9) is pleased to announce results from the next phase of its Project Enhancement Options within its independently prepared Preliminary Economic Assessment (PEA) for the Livengood Gold Project, Alaska. Management anticipates continuing to refine and improve project economics as additional information becomes available. The results from this phase of the Company's PEA report highlight two important alternatives under consideration for the potential development of the Livengood gold deposit. All references to monies in this news release are to US dollars unless otherwise indicated.

The first alternative outlines an initial low capex, accelerated heap leach only option which could provide cash flow to support the development of a large mill phase for the project (Tables 1 & 2). The second alternative looks at expanding the projected milling circuit which benefits the project through economies of scale, increased production and compressed mine life (Tables 3 & 4). These alternatives offer significant enhancement to the base case plan presented in ITH's August 3, 2010 news release and point to the significant potential that the large Livengood deposit has for further optimization.

The heap leach only option is emerging as a highly attractive initial stage for ITH because it is a simpler project from the permitting, process, construction and operational standpoints, all of which can be accelerated. This alternative also has much lower capex and operating costs, which produces a compelling internal rate of return, NPV and annual gold production. The large mill-heap option reflects overall project value and has significant leverage to gold price.

Jeffrey Pontius, President and CEO, stated "The option analysis has highlighted not only a strategic path forward for ITH's development of the Livengood project but also the value potential of this new world class gold discovery. As the Company focuses on optimizing the development of Livengood with the reduced capex, accelerated plan for heap leaching, we will also be continuing to examine other options, such as a simple, heap compatible mill, to address the deposit's emerging contiguous higher grade zones. The analysis of this and other options are currently in full swing as the project begins the optimization phase."

Table 1

Livengood Project -- Heap Leach Only Option - PEA Summary

(all values in 2010 USD based on an $775 pit shell, mining recoverable in-pit resources above 0.3 g/t gold cut off)

| In-pit resource - Indicated |

251Mt @ 0.62 g/t gold for 5.03M contained ounces gold,

3.54M recoverable ounces gold |

| In-pit resource - Inferred |

9 Mt @ 0.54 g/t gold for 0.15M contained ounces gold,

0.11M recoverable ounces gold |

| NPV(5%) and IRR at USD 950 per Oz |

USD 579M; 26.9% |

| Over all strip ratio of : |

1 to 1.1 (mined mineral resource to waste) |

| Average Annual gold production: |

513,000 ounces over a 7.1 year mine life |

| Average gold recovery: |

71% |

| Average LOM Mining rate: |

100,000 mined mineral resource tonnes per day,

210,000 total tonnes per day |

| Mining cost per/tonne: |

$1.45 |

| Heap Leach Processing cost/tonne |

$3.11 |

| G&A cost per processed tonne: |

$0.81 |

| Operating Cost per ounce: |

$486 |

| Initial capital cost*: |

$ 638 M |

| Life of mine sustaining capital costs: |

$154 M |

| Capital Contingency: |

20% |

* excludes working capital and initial fills/spare parts inventory

The Company will file the final version of an update of the NI 43-101 technical report which will include the results of this Preliminary Economic Analysis (the "Report") on SEDAR by September 17, 2010, and investors are urged to review the Report in its entirety.

Table 2

Heap Leach Only Option Gold Price Sensitivity Analysis

(all values in constant 2010 US$)

| Gold Price |

NPV(5%) ($M) |

NPV(7.5%) ($M) |

IRR (%) |

| $950 |

$579 |

$456 |

26.9% |

| $1,100 |

$988 |

$813 |

40.0% |

| $1,200 |

$1,260 |

$1,051 |

47.4% |

| $1,500 |

$2,077 |

$1,764 |

68.4% |

Table 3

Livengood Project -- Large Mill - Heap Leach PEA Summary

(all values in 2010 USD based on an $850 pit shell, mining recoverable in-pit resources above 0.3 g/t gold cut off)

| In-pit resource - Indicated |

600 Mt @ 0.65 g/t gold for 12.6M contained ounces gold,

9.8M recoverable ounces gold |

| In-pit resource - Inferred |

48 Mt @ 0.64 g/t gold for 1.0M contained ounces gold,

0.8M recoverable ounces gold |

| NPV(5%) and IRR at USD 950 per Oz |

USD 1.11B; 18.5% |

| Over all strip ratio of : |

1 to 1.07 (mined mineral resource to waste) |

| Average Annual gold production: |

833,000 ounces over a 12.6 year mine life |

| Average gold recovery: |

78% (73% Heap & 81% Mill) |

| Average LOM Mining rate: |

135,000 mined mineral resource tonnes per day,

280,000 total tonnes per day |

| Mining cost per/tonne: |

$1.41 |

| Mill Processing cost/tonne: |

$7.46 |

| Heap Leach Processing cost/tonne |

$2.84 |

| G&A cost per processed tonne: |

$0.59 |

| Operating Cost per ounce: |

$534 |

| Initial capital cost*: |

$ 625 M |

| Mill & Heap expansion capital cost |

$1,027 M |

| Life of mine sustaining capital costs: |

$579 M |

| Capital Contingency: |

25% |

* excludes working capital and initial fills/spare parts inventory

Table 4

Large Mill-Heap Option Gold Price Sensitivity Analysis

(all values in constant 2010 US$)

| Gold Price |

NPV(5%) ($M) |

NPV(7.5%) ($M) |

IRR (%) |

| $950 |

$1,113 |

$760 |

18.5% |

| $1,100 |

$2,147 |

$1,611 |

29.3% |

| $1,200 |

$2,837 |

$2,178 |

35.9% |

| $1,500 |

$4,906 |

$3,879 |

54.4% |

This PEA utilized preliminary estimates of heap leach and mill recovery, assuming a nominal 73% and 81% process recovery, respectively, for the large milling-heap leach option and an average of 71% for the heap leach only option (includes some minor lower recovery sulphide material in the pit design which would have gone to the mill in the combined study). The estimated mill recovery is consistent with the high average recovery (89%) of gold to concentrate demonstrated in the existing metallurgical testing data and the subsequent total gold recovery by CIL treatment in some of the mined mineral resource types.

Metallurgical testing will be conducted as part of a Pre-feasibility Study to verify the total gold recovery assumptions and to support design of the required mill and heap leach processes.

Carl Brechtel, Chief Operating Officer, stated "The very attractive early stage oxide heap leach project provides a strong base for our Company to begin enhancing the operational planning and economics. This work will focus on advancing both production and grade in the plan while looking for the most economically favourable development strategy that can minimize and mitigate the project's environmental impacts. The size and character of the Livengood deposit will enable the Company to look at a variety of project enhancement options as we progress toward a final design."

The Company cautions that this PEA is preliminary in nature, and is based on technical and economic assumptions which will be evaluated in the Pre-feasibility Study. The PEA is based on the Livengood in-situ resource model (June, 2010) which consists of material in both the indicated and inferred classification. Inferred mineral resources are considered too speculative geologically to have technical and economic considerations applied to them. The current basis of project information is not sufficient to convert the in-situ mineral resources to mineral reserves, and mineral resources that are not mineral reserves do not have demonstrated economic viability. Accordingly, there can be no certainty that the results estimated in this PEA will be realized. The PEA results are only intended as an initial, first-pass review of the potential project economics based on preliminary information.

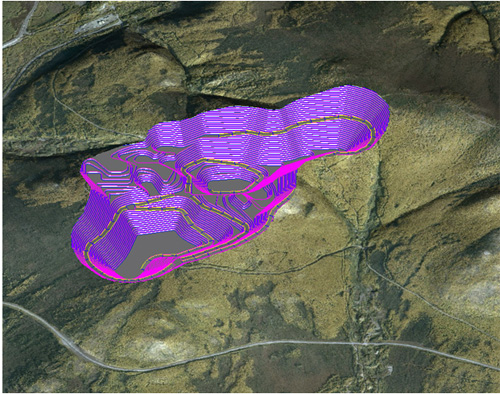

This Livengood PEA utilizes the June 2010 in-situ resource estimate, which includes all assays completed through May, 2010 (434 diamond and reverse circulation holes). The mine production estimate was developed by incremental revenue optimization to produce a series of pit shells defined at varying gold prices between $300 and $1500 per ounce, for the gold recovery and processing cost assumptions. A long term gold price of $950 per gold ounce has been assumed in this PEA, and the pit shells, defined at $775 and $850 per gold ounce, were selected for the analysis to assure a minimum margin on process cost of greater than $100 per gold ounce. The resulting pit design for the combined heap leach and mill option at projected full extraction is shown in Figure 1, and a series of 5 push-backs were chosen within the shell as the basis of a production schedule that would deliver a nominal 135,000 tonnes/day mined mineral resource output. Individual in-situ resource blocks within the pit shell were assigned an economic value based on recovery and contained gold above the 0.3 g/t cut-off grade, and the blocks were assigned to one of the heap leach, mill or waste dump destinations based on the economic value. For blocks assigned to the heap leach or mill destination, the individual block grade-tonnage data developed in the Multiple Indicator Kriging in-situ resource model was used to calculate the mining recoverable tonnage above the 0.3 g/t cut-off grade. The mining recoverable resource was scheduled to the appropriate process circuit (mill or heap leach) and the remaining material below the 0.3 g/t cut-off was scheduled to the waste rock storage facility.

The Livengood mineralization remains open in a number of directions particularly to the west, southeast and at depth. The Company is continuing its resource expansion drilling campaign which is focused on expanding the higher grade Southwest Zone of the deposit, confirming the inferred resource extrapolation at depth, and infilling the drill pattern to increase the drill density in the core of the Sunshine Zone and Main Zone mineralization.

Figure 1: Geo-referenced surface photography of the Livengood area showing the $850 pit defined by incremental revenue optimization using the Livengood June 2010 in-situ resource model. The route of the paved, Elliot highway is shown below the projected crest of the open pit.

Cash Flow Model Inputs and Assumptions

Resources - The analysis included both indicated and inferred resources in the mining and economic study. Indicated resources make up more than 90% of the defined in-pit mineral resource tonnage.

Mining Method - A standard open pit drill, blast, load and haul mining plan was used for the study, assuming a 45o pit slope. Designs for pit roads and ramps have been developed, and the schedule includes the additional waste tonnage required. The assumed nominal mining rate was 210,000 and 280,000 total tonnes per day for the heap leach only and mill heap leach combination, respectively (365 operating days per year).

Heap Leach Processing Method - A valley fill heap leach design, initially operated at 100,000 tonnes of mined mineral resource a day, was assumed for the PEA heap leach only option. The mined mineral resource to be heap leached would be crushed to 1.2 cm and truck stacked on the pad.

Combined Heap Leach -- Mill Processing Method -- A valley fill heap leach design, initially operated at 100,000 tonnes of mined mineral resource a day and declining to nominal 89,000 tonnes of mined mineral resource per day for the first 6 years after the mill start-up in year 4, was assumed for the PEA. The mined mineral resource to be heap leached would be crushed to 1.2 cm and truck stacked on the pad. A process plant using SAG milling, gravity and flotation circuits for concentration and CIL recovery of gold was assumed in the PEA. The process plant was assumed to have a nominal throughput of 100,000 tonnes per day, beginning operation in year 4, after 3 years of heap leach processing.

Gold Recovery Model - Process recoveries were estimated for each of 21 different mineralization types (7 rock types, 3 oxidations states) in the deposit based on metallurgical test results published in the June 2010 update of the Livengood technical data. The quantity of mineralization types are then projected into the in-situ resource block model using a 3D geological model of the deposit, and a process recovery factor is calculated for each model block. The calculated process recovery factor is used to determine produced gold ounces for the portion of mine recoverable material above the 0.3 g/t cut-off grade for each block according to its processing destination (heap leach or mill).

Operating and Capital Cost Estimates - Preliminary capital and operating costs were prepared using information available on other Alaskan gold mines, an independent mining and development cost research report commissioned by the Company, all available project technical data and metallurgical/process related test work, as well as project site reviews by the independent consultants and the Qualified Persons authoring the Report. Preliminary site infrastructure alternatives (heap leach, waste dump, tailing storage facilities, and mill) have been evaluated by independent study and an arrangement defined as the basis of capital cost estimates. Capital costs for the combined heap leach -- mill option were estimated from a review of recent gold projects developed in the region. Capital costs were developed based on a nominal mining rate of 135,000 tonnes of mined mineral resource per day (nominal total tonnes mined per day of 280,000), processing a total of 650 Mt, and includes sustaining capital and all facilities and equipment needed for all phases of the project over its projected 12.6 year life. Capital costs for the heap leach only option were estimated from a review of recent gold projects developed in the region. Capital costs were developed based on a nominal mining rate of 100,000 tonnes of mined mineral resource per day (nominal total tonnes mined per day of 210,000), processing a total of 259 Mt, and includes sustaining capital and all facilities and equipment needed for all phases of the project over its projected 7.1 year life. All costs are in constant USD from Q3 2010. No escalation was applied in the financial models.

Taxes and Royalties - Taxes and royalty charges were excluded from this preliminary analysis of the project. Net smelter return royalty rates vary from 0-5% across the project and average approximately 2.5%, assuming exercise by the Company of all available royalty buy-out rights.

Revenue - Revenue was determined in the base case financial model assuming a constant, long term gold price of $950 per Au ounce. All sensitivities to gold price assumptions were assessed using a constant price.

June 2010 Resource Update

Reserva International, LLC. produced an updated in-situ mineral resource estimate, the results of which were included in the June 2010 update of the Livengood NI 43-101 (June 2010 Summary Report on the Livengood Project, Tolovana District, Alaska). Summary results at different cut-off grades are listed in Tables 5, 6 and 7. This in-situ resource estimate was used as the basis for the Mill and Heap Leach PEA.

Table 5

June 2010 Livengood Resources (at 0.30 g/t gold cutoff)

| Classification |

Gold Cutoff

(g/t) |

Tonnes

(millions) |

Gold

(g/t) |

Million Ounces Gold |

| Indicated |

0.30 |

789 |

0.62 |

15.7 |

| Inferred |

0.30 |

229 |

0.55 |

4.0 |

Table 6

June 2010 Livengood Resources (at 0.50 g/t gold cutoff)

| Classification |

Gold Cutoff

(g/t) |

Tonnes

(millions) |

Gold

(g/t) |

Million Ounces Gold |

| Indicated |

0.50 |

409 |

0.83 |

10.9 |

| Inferred |

0.50 |

94 |

0.79 |

2.4 |

Table 7

June 2010 Livengood Resources (at 0.70 g/t gold cutoff)

| Classification |

Gold Cutoff

(g/t) |

Tonnes

(millions) |

Gold

(g/t) |

Million Ounces Gold |

| Indicated |

0.70 |

202 |

1.07 |

6.9 |

| Inferred |

0.70 |

40 |

1.06 |

1.4 |

The scale of the Livengood gold system is demonstrated by the size of the estimated resource using a 0.3 g/t gold cutoff (Table 5). This resource forms a coherent body covering a lateral extent of three square kilometres and remains open in several directions.

The resource model for the deposit was developed using Multiple Indicator Kriging techniques. Indicator variogram modeling was done on 10 metre composites. The resource model was constrained by the lithological model developed by the Company. Spatial statistics indicate that the mineralization shows very reasonable continuity within the range of anticipated operational cutoffs. Bulk density was estimated on the basis of individual density measurements made on core samples and reverse circulation drill chips from each stratigraphic unit. In total, 98 measurements were used. Block density was assigned on the basis of the lithological model. The resource model, with blocks 15 x 15 by 10 metres, was estimated using nine indicator thresholds. A change-of-support correction was imposed on the model assuming 5 x 5 x 10 metre selectable mining units. Classification of indicated and inferred was based on estimation variance.

Livengood Project Highlights

- Drilling at the project continues to expand the deposit in several directions; at depth, to the west in the Lillian area and to the southeast in the Sunshine Zone.

- The Company has begun the Money Knob pre-feasibility study with the initiation of hydrological studies, surface mine facility location analysis, phase 2 metallurgical studies, deposit scale geotechnical studies, condemnation drilling and the continuing collection of environmental baseline data.

- Ongoing metallurgical studies continue to focus on column leach testing for heap leaching process design, and on gravity and flotation concentration, which has returned initial average recoveries to concentrate of 89% and offers a significant potential for operational and capital cost savings. Optimization work is ongoing for these processing alternatives, as they have potential to make significant positive impacts on project economics.

- The geometry of the currently defined shallowly dipping, outcropping deposit has a low strip ratio amenable to low cost open pit mining which could support a high production rate and economies of scale. Future mining studies will continue to evaluate mining and processing production rates as well as the possible introduction of a smaller mill into the heap leach only option which recombines mill tails with heap material for additional extraction during the heap leach process on the leach pad.

- The Livengood project has a very favourable logistical location, being situated 110 road kilometres north of Fairbanks, Alaska along the paved, all-weather Elliott Highway, the Trans-Alaska Pipeline Corridor, and the proposed Alaska natural gas pipeline route. The terminus of the Alaska State power grid lies approximately 80 kilometres to the south.

- ITH controls 100% of its approximately 145 square kilometre Livengood land package, which is made up of fee land leased from the Alaska Mental Health Trust, a number of smaller private mineral leases and 115 Alaska state mining claims.

- No major permitting hurdles have been identified to date.

Geological Overview

The Livengood Deposit is hosted in a thrust-interleaved sequence of Proterozoic to Paleozoic sedimentary and volcanic rocks. Mineralization is related to a 90 million year old (Fort Knox age) dike swarm that cuts through the thrust stack. Primary mineralization controls are a combination of favourable lithologies and crosscutting structural zones. In areas distal to the main structural zones, the selective development of disseminated mineralization in favourable host rocks is the main mineralization control. Within the primary structural corridors, all lithologies can be pervasively altered and mineralized. Devonian volcanic rocks and Cretaceous dikes represent the most favourable host lithologies and are pervasively altered and mineralized throughout the deposit. Two dominant structural controls are present: 1) the major shallow south-dipping faults which host dikes and mineralization which are related to dilatant movement on structures of the original fold-thrust architecture during post-thrusting relaxation, and 2) steep NW trending linear zones which focus the higher-grade mineralization which cuts across all lithologic boundaries. The net result is broad flat-lying zones of stratabound mineralization around more vertically continuous, higher grade core zones with a resulting lower strip ratio for the overall deposit and higher grade areas that could be amenable for starter pit production.

The surface gold geochemical anomaly at Livengood covers an area 6 kilometres long by 2 kilometres wide, of which approximately half has been explored by drilling to date. Surface exploration is ongoing as new targets are being developed to the northeast and west of the known deposit.

Qualified Persons and Quality Control/Quality Assurance

Tim Carew, P.Geo., of Reserva International, LLC., a mining geo-scientist, is a Professional Geoscientist in the province of British Columbia (No. 18453) and, as such, has acted as the Qualified Person, as defined in NI 43-101, for the June 2010 resource modeling for the Livengood deposit. Mr. Carew has a B.Sc. degree in Geology, an M.Sc in Mineral Production Management and more than 34 years of relevant geological and mining engineering experience in operating, corporate and consulting environments. Both Mr. Carew and Reserva International, LLC. are independent of the Company under NI 43-101.

Dr. Paul D. Klipfel, Ph.D., AIPG, a consulting economic geologist employed by Mineral Resource Services Inc., has acted as the Qualified Person, as defined in NI 43-101, for the exploration data and supervised the preparation of the technical exploration information on which some of this news release is based. Dr. Klipfel has a PhD in economic geology and more than 28 years of relevant experience as a mineral exploration geologist. He is a Certified Professional Geologist [CPG 10821] by the American Institute of Professional Geologists. Both Dr. Klipfel and Mineral Resource Services Inc. are independent of the Company under NI 43-101.

Mr. William J. Pennstrom, Jr., of Pennstrom Consulting Inc., a consulting metallurgical engineer, is acting as the Qualified Person, as defined in NI 43-101, for the metallurgy and mineral processing programs for the Livengood deposit, and development of the PEA project financial analysis. Mr. Pennstrom has a BS degree in Metallurgical Engineering and a Masters degree in Business Management. He has more than 26 years of relevant experience as a metallurgist, having functioned as an operator, engineer, and process consultant over this time frame. Mr. Pennstrom is also a Qualified Professional (QP) member of the Mining and Metallurgical Society of America. Both Mr. Pennstrom and Pennstrom Consulting Inc. are independent of the Company under NI 43-101.

Mr. Quinton de Klerk, Director of Mining Solutions at Cube Consulting, Perth Australia, is a consulting mining engineer specializing in open pit design, open pit optimization and analysis, mine design, production scheduling, due diligence evaluations and mineral reserves reporting. He is acting as Qualified Person, as defined in NI 43-101, for the open pit optimization and scheduling work for the Livengood Deposit. Mr. de Klerk has over 15 years experience in open pit mining and is a Corporate Member of AusIMM. He holds a Mine Manager's Certificate in South Africa and a National Higher Diploma in Metalliferous Mining. Both Mr. de Klerk and Cube Consulting are independent of the Company under NI 43-101.

Mr. John Bell, Sr. Project Manager at MTB Project Management Professionals, Inc of Denver, Colorado, is a graduate civil engineer, with an MBA, specializing in project management, cost estimation, project controls, construction management and contract administration. Mr. Bell is acting as Qualified Person, defined in NI 43-101, for capex and opex cost review for the Livengood Project. Mr. Bell has over 46 years experience working in the engineering and construction industry in North and South America, Europe, Australia and Asia. He is a Life Member of the American Society of Civil Engineers, a member of the Association for Advancement of Cost Engineering, a member of the Institution of Engineers, Australia and a Chartered Professional Engineer in Australia (#172814). Both Mr. Bell and MTB Project Management Professionals, Inc. are independent of the Company under NI 43-101.

Jeffrey A. Pontius (CPG 11044), a qualified person as defined by National Instrument 43-101, has supervised the preparation of the scientific and technical information that forms the basis for this news release and has approved the disclosure herein. Mr. Pontius is not independent of ITH, as he is the President and CEO and holds common shares and incentive stock options.

Development work at the Livengood Project is directed by Carl E. Brechtel (Colorado PE 23212, Nevada PE 8744), who is a qualified person as defined by National Instrument 43-101. He is a graduate geological engineer with an MS degree in mining engineering. He is a member of the Society for Mining, Metallurgy and Exploration located in Denver CO, AusIMM (Australia) and SAIMM (South Africa). Mr. Brechtel has supervised the preparation of the technical and economic information that forms the basis for this news release and has approved the disclosure herein. Mr. Brechtel is not independent of ITH, as he is the COO and holds incentive stock options.

The work program at Livengood was designed and is supervised by Chris Puchner, Chief Geologist (CPG 07048), of the Company, who is responsible for all aspects of the work, including the quality control/quality assurance program. On-site personnel at the project photograph the core from each individual borehole prior to preparing the split core. Duplicate reverse circulation drill samples are collected with one split sent for analysis. Representative chips are retained for geological logging. On-site personnel at the project log and track all samples prior to sealing and shipping. All sample shipments are sealed and shipped to ALS Chemex in Fairbanks, Alaska for preparation and then on to ALS Chemex in Reno, Nevada or Vancouver, B.C. for assay. ALS Chemex's quality system complies with the requirements for the International Standards ISO 9001:2000 and ISO 17025:1999. Analytical accuracy and precision are monitored by the analysis of reagent blanks, reference material and replicate samples. Quality control is further assured by the use of international and in-house standards. Finally, representative blind duplicate samples are forwarded to ALS Chemex and an ISO compliant third party laboratory for additional quality control.

About International Tower Hill Mines Ltd.

International Tower Hill Mines Ltd. is a resource exploration company focused on the ongoing development of the advanced, multimillion-ounce gold discovery at Livengood in Alaska. ITH is

committed to the aggressive development of the Livengood Project, thereby giving its shareholders the maximum value for their investment.

On behalf of

INTERNATIONAL TOWER HILL MINES LTD.

(signed) Jeffrey A. Pontius

Jeffrey A. Pontius,

President and Chief Executive Officer

Contact Information:

Quentin Mai, Vice-President - Corporate Communications

E-mail: [email protected]

Phone: 1-888-770-7488 (toll free) or (604)683-6332 / Fax: (604) 408-7499

Shirley Zhou, Manager - Corporate Communications

Email: [email protected]

Phone: 1-888-770-7488 (toll free) or (604) 638-3246 / Fax: (604) 408-7499

Cautionary Note Regarding Forward-Looking Statements

This press release contains forward-looking statements and forward-looking information (collectively, "forward-looking statements") within the meaning of applicable Canadian and US securities legislation. All statements, other than statements of historical fact, included herein including, without limitation, statements regarding the anticipated content, commencement and cost of exploration programs, anticipated exploration program results, the discovery and delineation of mineral deposits/resources/reserves, the potential for the expansion of the estimated resources at Livengood, the potential for any production at the Livengood project, the potential for higher grade mineralization to form the basis for a starter pit component in any production scenario, the potential low strip ratio of the Livengood deposit being amenable for low cost open pit mining that could support a high production rate and economies of scale, the potential for cost savings due to the high gravity concentration component of some of the Livengood mineralization, the completion of a pre-feasibility study at Livengood, the potential for a production decision to be made regarding Livengood, the potential commencement of any development of a mine at Livengood following a production decision, business and financing plans and business trends, are forward-looking statements. Information concerning mineral resource estimates and the preliminary economic analysis thereof also may be deemed to be forward-looking statements in that it reflects a prediction of the mineralization that would be encountered, and the results of mining it, if a mineral deposit were developed and mined. Although the Company believes that such statements are reasonable, it can give no assurance that such expectations will prove to be correct. Forward-looking statements are typically identified by words such as: believe, expect, anticipate, intend, estimate, postulate and similar expressions, or are those, which, by their nature, refer to future events. The Company cautions investors that any forward-looking statements by the Company are not guarantees of future results or performance, and that actual results may differ materially from those in forward looking statements as a result of various factors, including, but not limited to, variations in the nature, quality and quantity of any mineral deposits that may be located, variations in the market price of any mineral products the Company may produce or plan to produce, the Company's inability to obtain any necessary permits, consents or authorizations required for its activities, the Company's inability to produce minerals from its properties successfully or profitably, to continue its projected growth, to raise the necessary capital or to be fully able to implement its business strategies, and other risks and uncertainties disclosed in the Company's Annual Information Form filed with certain securities commissions in Canada and the Company's annual report on Form 20-F filed with the United States Securities and Exchange Commission (the "SEC"), and other information released by the Company and filed with the appropriate regulatory agencies. All of the Company's Canadian public disclosure filings may be accessed via www.sedar.com and its United States public disclosure filings may be accessed via www.sec.gov, and readers are urged to review these materials, including the technical reports filed with respect to the Company's mineral properties.

Cautionary Note Regarding References to Resources and Reserves

National Instrument 43 101 - Standards of Disclosure for Mineral Projects ("NI 43-101") is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all resource estimates contained in or incorporated by reference in this press release have been prepared in accordance with NI 43-101 and the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the "CIM") Standards on Mineral Resource and Mineral Reserves, adopted by the CIM Council on November 14, 2004 (the "CIM Standards") as they may be amended from time to time by the CIM.

United States shareholders are cautioned that the requirements and terminology of NI 43-101 and the CIM Standards differ significantly from the requirements and terminology of the SEC set forth in the SEC's Industry Guide 7 ("SEC Industry Guide 7"). Accordingly, the Company's disclosures regarding mineralization may not be comparable to similar information disclosed by companies subject to SEC Industry Guide 7. Without limiting the foregoing, while the terms "mineral resources", "inferred mineral resources", "indicated mineral resources" and "measured mineral resources" are recognized and required by NI 43-101 and the CIM Standards, they are not recognized by the SEC and are not permitted to be used in documents filed with the SEC by companies subject to SEC Industry Guide 7. Mineral resources which are not mineral reserves do not have demonstrated economic viability, and US investors are cautioned not to assume that all or any part of a mineral resource will ever be converted into reserves. Further, inferred resources have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. It cannot be assumed that all or any part of the inferred resources will ever be upgraded to a higher resource category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of a feasibility study or prefeasibility study, except in rare cases. The SEC normally only permits issuers to report mineralization that does not constitute SEC Industry Guide 7 compliant "reserves" as in-place tonnage and grade without reference to unit amounts. The term "contained ounces" is not permitted under the rules of SEC Industry Guide 7. In addition, the NI 43-101 and CIM Standards definition of a "reserve" differs from the definition in SEC Industry Guide 7. In SEC Industry Guide 7, a mineral reserve is defined as a part of a mineral deposit which could be economically and legally extracted or produced at the time the mineral reserve determination is made, and a "final" or "bankable" feasibility study is required to report reserves, the three-year historical price is used in any reserve or cash flow analysis of designated reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

This press release is not, and is not to be construed in any way as, an offer to buy or sell securities in the United States. |